Reserve funds are a long-established way for municipalities to manage money. As of September 30th, 2025, Burlington’s reserve funds held $223.5 million, of which $90.2 million is what the city calls committed, meaning the city knows how the money will be spent.

Burlington receives money from a variety of sources, including taxpayers, user fees, other levels of government, and even private donations. Every year, some of this money is funnelled into reserve funds. Reserve funds serve to buffer or spread-out large expenditures over many years. Ultimately, the money in reserve funds belongs to taxpayers, as the majority of it was collected from them.

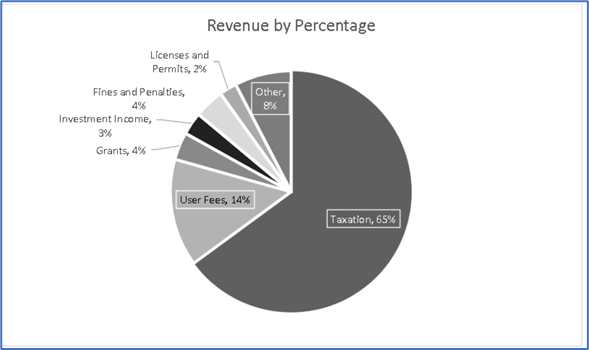

This pie chart shows Burlington’s revenue sources in 2024. (December 31, 2024).

There are four basic types of reserve funds:

1. Stabilization Reserves (The “Rainy Day” Fund)

This type of fund is intended to offset unexpected revenue shortfalls (fewer new homes were built, and started paying property taxes, than the city expected) or emergency costs (for example, flooding).

Examples:

Burlington has a tax rate stabilization reserve fund. In 2022, the city drew approximately $2.3 million from its Tax Rate Stabilization Reserve Fund to help offset COVID-19 impacts on the operating budget.

Burlington also has a severe weather reserve fund. The city budgets for snow clearing, but some winters are worse than others. The severe weather reserve is used to cover additional costs during a bad winter and is topped up during a mild winter.

2. Capital Reserve Fund (Asset Replacement)

This is typically the most significant portion of a municipality’s reserves. Capital reserves are intended to fund the replacement of roads, pipes, and buildings.

For example, responsibility for the roads in a small area of Alton Village has recently been transferred from the developer to the city. The city can expect those roads to need replacement in about 30 years. Each year, a small portion of the property taxes paid by residents in that area of Alton Village should be set aside to fund the road replacement. Thirty years from now, the money to rebuild the road will be “in the bank” or, more correctly, in a reserve fund.

In reality, we all contribute to a group or large reserve funds to cover the cost of replacing infrastructure as required over time. There is no specific fund for the roads in Alton Village.

Burlington refers to this group of reserve funds as “CAPITAL RELATED RESERVE FUNDS AND RESERVES”. Every asset should be covered, from transit buses to storm sewers to community centres.

3. Contingency Reserves (Self Insurance)

Most Ontario employers are required to pay the Workplace Safety Insurance Board (WSIB) to manage costs associated with workplace illness and injuries. Some municipalities, including Burlington, choose to manage this insurance themselves. Contingency reserves are funds set aside to cover insurance claims for employees’ workplace-related injuries and illnesses.

Contingency reserve funds are also used for post-employment benefits. Retiring city employees receive a defined benefit, inflation-protected pension plan from OMERS, along with health benefits from the city. As the number of employees increases, so will the number of retirees collecting benefits. Contributions to this contingency reserve can be made annually to fund future benefit liabilities, rather than leaving those liabilities for a future generation of taxpayers.

4. Obligatory Reserve Funds

These are provincially legislated funds that must be segregated from other funds and used only for their prescribed purpose. Examples are:

- Development charges

- Cash In Lieu of Parkland

- Gas tax reserve funds

The Development Charges (DC) Reserve Fund is used to ensure that “growth pays for growth.” When new homes or businesses are built, developers pay fees that are held in this fund to pay for new infrastructure and services required to support the increased population. New developments in Burlington allow more people to live in the city. The Burlington Public Library receives $60,000 annually from this fund to purchase new books to serve a growing population.

Just how reserved is Burlington?

Money regularly flows in and out of reserve funds.

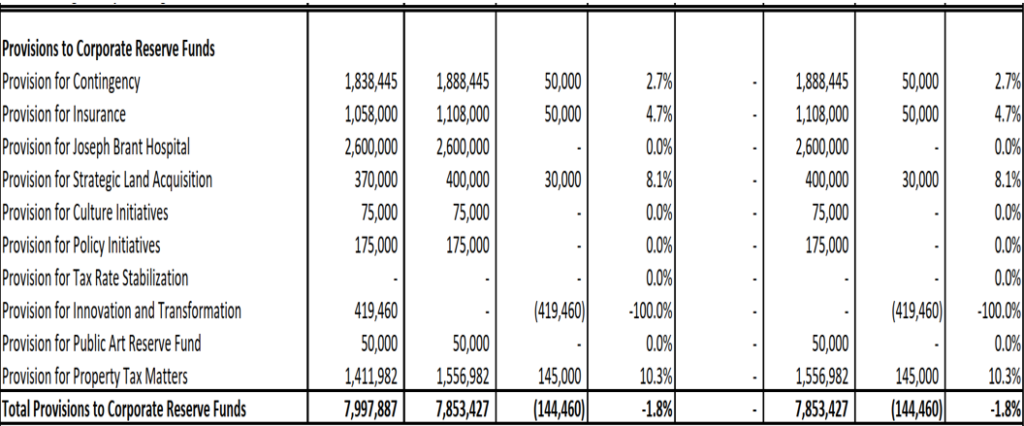

The 2026 budget shows that $7,997,887 will be transferred into the following reserve funds.

Many of the budgeted expenses for 2026 will draw on reserves.

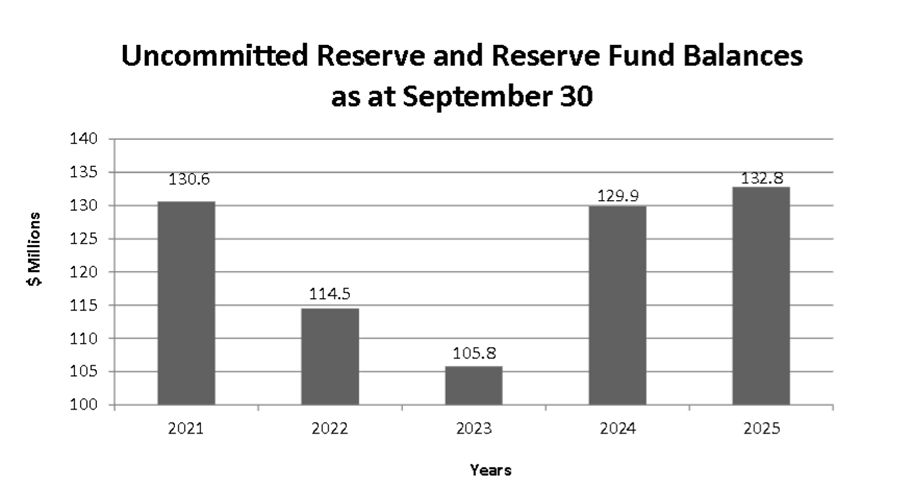

This chart shows uncommitted reserve funds over time (as of September 30th, 2025).

In 2015, the Ontario government introduced rules requiring municipalities to use a standardized, evidence-based approach to asset management. The city’s asset management plan tracks each asset and predicts when the asset will need replacement. Using an asset management plan, the city can forecast the costs of replacement or overhaul. The province does not set specific lifespans for assets; for example, Ontario doesn’t require that Art Galleries be rebuilt every fifty years. It’s up to individual municipalities to set an asset’s lifespan. Ontario’s law requires Burlington to demonstrate a lifecycle strategy that identifies the most cost-effective way to keep the asset running, through maintenance, repair, or full replacement.

These are common guidelines:

| Asset Type | Typical Useful Life (Est.) |

| Asphalt Road (Local) | 15 – 25 years |

| Bridges (Concrete/Steel) | 50 – 75 years |

| Concrete Sidewalks | 30 – 50 years |

| Municipal Buildings | 40 – 60 years |

| Water/Sewer Pipes | 50 – 80 years |

The average age of a home in Burlington is approximately 45 years. The common guidelines shown above may overlook the fact that maintaining and occasionally renovating can be far less expensive than rebuilding.

What does Burlington’s Asset Management Plan Tell Us?

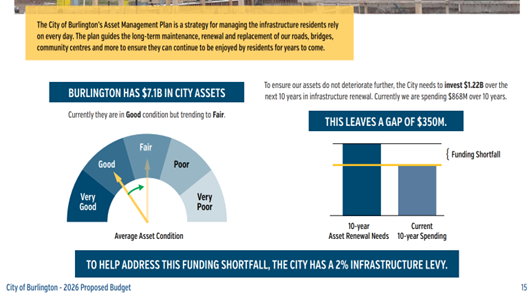

Page 15 of the budget talks about the need to invest $1.22 billion over the next ten years, while the city’s budget and reserve funds only support $868 million in spending over the next ten years. Based on a complex analysis of individual city assets, Burlington is not sufficiently reserved.

More information about the asset management plan is available here:

How much is too much?

Without delving into all the details of the asset management plan and challenging specific items, Burlington doesn’t have sufficient reserves to maintain its assets in a “State of Good Repair.”

Discover more from Focus Burlington

Subscribe to get the latest posts sent to your email.

Is it the author’s position that the city doesn’t have sufficient funds to maintain the AMP or just what was gleaned from the city’s position on the matter?

The city owns many assets which make up the infrastructure of the city. These asset categories are Corporate Facilities, Corporate Fleet, Fire, IT, Parking, Parks, Recreation which includes Community and Culture, Stormwater, Transit, Transportation, and Urban Forestry. The lifespan of assets is different for each category but only 3 have 10 year lifespans with the rest being 30-110 years. Assets are ranked as being in very poor, poor, fair, good or very good condition. As per the city’s Asset Management Plan or AMP, 85% of the city’s assets were classed in fair, good or very good condition at the end of 2021. With the efforts of council we would assume this has further improved. In the 2021 AMP the average age of assets was 6-37 years old. Therefore, most of these assets are in good shape, relatively new and years from needing replacement.

It was actually 91.1% of assets classed as fair or better but in 2023 the replacement value of the assets was prematurely restated by from 5.3B to 6.3B dollars specifically for the 2024 budget. This was despite the reassessment not being required until 2028. Despite it only being a book entry, adding 1 Billion dollars to the stated value of assets has a substantial impact.

The finance department used numbers from 2020-2022 and covid as a basis for the decision citing higher costs from increased construction demand and labour shortages. Except covid was a once in a lifetime anomaly and by the release of the 2024 budget work forces and the economy had returned to normal. These factors they’d cited had not only stabilized but pressures from labour shortages, construction demands and higher prices, had resolved and returned to baseline prices.

The Bank of Canada had been addressing economic effects by raising interest rates since March 2022. The central bank raises the cost of borrowing to discourage spending to reduce demand and put downward pressure on prices. At the time of the 2024 budget we were in a technical recession with a weak economy and the full effects of the interest hikes had not yet been felt. The Bank of Canada was voicing concerns about market instability from homeowners not being able to afford mortgages at the current higher interest rates. In my delegation on this matter I pointed out that it was highly anticipated that interest rate cuts would occur as early as April 2024. The rate cuts actually began in June and continued throughout 2024 with the Bank of Canada rate falling from 5.00% to 3.25%, a significant drop. The Bank of Canada continued with cuts throughout 2025 and the rate currently sits at 2.25%

All of these facts support the position I put forth on Nov 23/2023 which was that the restated book value was premature and completely unnecessary. Further as stated herein, by law the re-evaluation of the assets was not legally required until 2028.

However by restating the book value of assets the city could collect more since taxing 6.3B generates more money that taxing 5.3B.

It is worth pointing out that this council made a pointed decision to accelerate funding for the AMP despite the fact that internal documents indicated there was not a fundamental necessity to do so. The city’s own internal documents stated, ““When considering the total quantity and value of assets the city owns, the backlog is not overly significant”. What this backlog referred to were the relatively small amount of assets that would be requiring repair or replacement in the near term. Again keeping in mind the asset management team had estimated 91.1% of assets in fair or better condition before the order to restate the value of the assets which dropped that down to 85% (bc 9.9%% of 6.3B is a bigger # than 9.9% of 5.3B)

Additionally, in the background information provided in that May report the document stated “It is important to note that the Asset Management Financing Plan is a long-term financial plan, and any progress made to reducing the funding gap occurs over time. The speed in which we make progress will largely depend on the city’s appetite for risk, willingness to pay, and changes to levels of service”.

Again, there was no legal requirement to restate the assets, to accelerate funding of the AMP and there wasn’t a significant number of assets that required immediate attention. Certainly not so much that it couldn’t have been addressed by the reserves on hand and the taxation collected thru the previous levies. In 2023 the levy was increased to 1.60%, part of the 7.52% property tax increase that year, as part of this desire by council to accelerate funding. Not because it was imperative to have it. Review of the AMP and by the city’s own documents, it was not necessary to do so. The city was also way ahead of its provincial requirements. But despite these facts, this council went to great lengths to convince the public increases to the DIR was needed by putting the fear of God into taxpayers that infrastructure was crumbling and they needed to act on it immediately. Despite internal documents saying quite the opposite.

If this council was engaging in this kind of truly bad faith rhetoric in 2023 and 2024, I wonder why if the author has done his own due diligence on this program & what this council claims it needs or if he is taking it on blind faith of their say so that we are still struggling to meet these purported shortfalls? The ones that didn’t exist when they put that fear of God into citizens so they’d swallow 7.52 (2023) and 7.82% (2024) tax increases (2024 ended up dropped to 6.68%).

Since taking a hiatus from politics to recover from an accident the last 1.5 yrs, I haven’t had an opportunity to reevaluate the AMP and related internal documents for that time span. But having seen this council sell residents a blatantly untrue story in 2023/24, and knowing that leopards can’t change their spots, I’d take this claim about shortfalls with a grain of salt. If there is a shortfall, its more likely from this council dipping into reserve funds to pay for interest on one of the several overpriced projects they’ve saddled taxpayers with. Or road work they’re suddenly doing in advance of an election to distract from what a truly fiscally irresponsible council they have been the last 8 years.

This article is an explanation of how reserve funds work in Burlington or any municipality and is intended as background information that may be referred to in future articles on this subject.